Info-Cafe

Results for : All categories

Results for : All categories

Basics of Limited Liability Partnership (LLP)

In India, businesses mainly operated as companies, sole proprietorships and partnerships. Each of these is subject to different regulatory and tax regimes reflecting their organization and ownership. With the growing Indian economy, the role played by its entrepreneurs as well as its technical and professional manpower has been acknowledged worldwide. Since then, a need was felt for a new corporate form that would provide an alternative to the traditional partnership, with unlimited personal liability on the one hand, and, the statute-based governance structure of the limited liability company on the other, in order to enable professional expertise and entrepreneurial initiative to combine, organize and operate in flexible, innovative and efficient way, which would provide a further impetus to India's economic growth. The limited liability partnership (abbreviated as 'LLP') is an answer to that.

After several deliberations and amendments by various committees, the revised Limited Liability Partnership Bill, 2008 was introduced in the Rajya Sabha on 21st October, 2008. After being passed by both Houses, the Honorable President of India gave assent to the Bill on 7th January 2009 and Limited Liability Partnership Act, 2008 ('The Act') became a law. The LLP in India is based on UK LLP Act, 2000 and Singapore LLP Act, 2005.

The LLP is an alternative corporate business vehicle that provides the benefits of limited liability of a company but allows its members the flexibility of organizing their internal management on the basis of a mutually arrived agreement, as is the case in a partnership firm.

The salient features of the LLP under the Act are as follows:

• The LLP is an alternative corporate business vehicle that gives the benefits of limited liability but would allow its members the flexibility of organizing their internal structure as a partnership based on an agreement amongst its partners.

• Since LLP contains elements of both 'corporate structure' as well as 'partnership firm structure' LLP is called a hybrid between a company and a partnership.

• The Act does not restrict the benefit of LLP structure to certain classes of professionals only and is available for use by any enterprise which fulfils the requirements of the Act.

• The LLP is a body corporate and a legal entity separate from its partners. Any two or more persons, associated for carrying on a lawful business with a view to profit, may by subscribing their names to an incorporation document and filing the same with the Registrar, form a LLP. It is capable of entering into contracts and holding property in its own name.

• The LLP has perpetual succession. The LLP can continue its existence irrespective of changes in partners.

• The mutual rights and duties of partners of an LLP inter se and those of the LLP and its partners are governed by an agreement between partners or between the LLP and the partners subject to the provisions of the proposed legislation. LLP provides flexibility to devise the agreement as per their choice. In the absence of any such agreement, the mutual rights and duties shall be governed by Schedule I to the Act.

• The LLP is a separate legal entity, liable to the full extent of its assets, with the liability of the partners being limited to their agreed contribution in the LLP which may be of tangible or intangible nature or both tangible and intangible in nature. No partner would be liable on account of the independent or unauthorized actions of other partners or their misconduct. The liabilities of the LLP and partners who are found to have acted with intent to defraud creditors or for any fraudulent purpose shall be unlimited for all or any of the debts or other liabilities of the LLP.

• Every LLP shall have at least two partners and shall also have at least two individuals as designated partners, of whom at least one shall be resident in India. The duties and obligations of designated partners shall be as provided in the Act read with the LLP agreement.

• The LLP shall be under an obligation to maintain annual accounts reflecting true and fair view of its state of affairs. A statement of accounts and solvency shall be filed by every LLP with the Registrar every year. The accounts of LLPs shall also be audited, subject to exemption to certain class of LLPs.

• The Central Government shall have powers to investigate the affairs of an LLP, if required, by appointment of competent inspector for the purpose.

• The compromise or arrangement including merger and amalgamation of LLPs shall be in accordance with the provisions of the Act.

• A firm, private company or an unlisted public company would be allowed to be converted into LLP in accordance with the provisions of the Act. Upon such conversion, on and from the date of certificate of registration issued by the Registrar in this regard, the effects of the conversion shall be such as are specified in the Act. On and from the date of registration specified in the certificate of registration, all tangible (movable or immovable) and intangible property vested in the firm or the company, all assets, interests, rights, privileges, liabilities, obligations relating to the firm or the company, and the whole of the undertaking of the firm or the company, shall be transferred to and shall vest in the LLP without further assurance, act or deed and the firm or the company, shall be deemed to be dissolved and removed from the records of the Registrar of Firms or Registrar of Companies, as the case may be.

• The winding up of the LLP may be either voluntary or by the National Company Law Tribunal.

• The Act confers powers on the Central Government to apply provisions of the Companies Act, 2013 as appropriate, by notification with such change s or modifications as deemed necessary. However, such notifications shall be laid in draft before each House of Parliament for a total period of 30 days and shall be subject to any modification as may be approved by both Houses.

• The Indian Partnership Act, 1932 is not applicable to LLPs.

• Taxation of LLP is akin to taxation of a partnership firm under the Income-tax Act, 1961.

Benefits to LLP under Income Tax Act, 1961 and Companies Act, 2013: There are several benefits to a LLP under the Income-tax Act, 1961 and the Companies Act 2013 over a company, the same is summarized below:

|

S. No. |

Features |

Company |

LLP |

|

1 |

Legal entity |

Separate |

Separate |

|

2 |

Perpetual succession |

Yes |

Yes |

|

3 |

Liability |

Limited |

Limited |

|

4 |

No. of members / partners |

Private company- Minimum: 2; Maximum:200 Minimum 2 Public company –Minimum: 7; Maximum: No limit One person company - 1 |

Minimum – 2 Maximum – No Limit |

|

5 |

Instrument requirements - Incorporation |

Memorandum and articles to be filed with RoC, Fees for filing all doc. Memorandum to be in respective forms specified in Tables A, B, C, D and E in Schedule I Articles to be in respective forms specified in Tables F,G,H,I and J in Schedule I Various other documents required to be filed at the time of incorporation. Filing Fee high as compared to LLP |

Incorporation documents to be filed with Registrar. LLP Agreement is to be filed with Registrar in Form 3. In absence of certain clauses in LLP Agreement, mutual rights and duties will be as specified in First Schedule to LLP Act. Filing Fee very less as compared to company |

|

6 |

One person formations |

One person can form a company under Companies Act, 2013 – One person company |

One person cannot form a LLP. |

|

7 |

Types of entities |

Companies Act, 2013 provides for various types of companies such as small company, dormant company, producer company, holding company, subsidiary company, associate company, etc. |

No different types, only one type LLP |

|

8 |

Change of registered office |

In case of change from one Registrar to another – prior approval from Regional Director required |

Registered office can be changed to any place in India by informing RoC subject to prescribed conditions. Less formalities as compared to company |

|

9 |

Suffix to the name |

Name to contain 'Limited' or 'Private Limited' as suffix |

Name to contain 'Limited Liability Partnership' or 'LLP' as suffix |

|

10 |

Bringing in capital |

Cumbersome process of Public Issue, Private Placement, Preferential Issue or Rights Issue |

Very easy to bring in capital |

|

11 |

Directors identity |

All directors to obtain director identification number (DIN) |

Only designated partners to obtain designated partners identification Number (DIN). |

|

12 |

Operations of business |

Regulated by memorandum and articles of association |

Regulated by LLP agreement |

|

13 |

Listing on stock exchanges |

Possible |

Not possible |

|

14 |

Meetings |

Regulated by Companies Act, 2013 – Board Meetings, general meetings are required. |

Not mandatory - No provision for regular Meeting of Board of partners. Partners can decide when and how to meet, delegation of powers etc. as per the LLP agreement. |

|

15 |

Statutory audit |

Compulsory even if no transaction during the year. |

Compulsory only if turnover exceeds Rs. 40 lakh or contribution exceeds Rs. 25 lakh |

|

16 |

Other audits |

Specified companies to have internal auditors, cost auditors, secretarial auditors. |

No such requirement under LLP Regulations |

|

17 |

Formats for Financial Statements |

It provides for specific format for financial statements. Non compliance results in heavy penalties |

No specific format under LLP Regulations |

|

18 |

Other Disclosures |

Detailed disclosures for annual reports, directors report, etc. |

No such provisions under LLP Regulations |

|

19 |

Method of accounting |

Accrual only |

Cash or accrual, any one allowed |

|

20 |

Day-to-day business operations |

Managing director, whole-time director and KMP to look after day-to-day administration |

Designated partner to look after statutory compliances. All partners can look into day-to-day affairs of the LLP as per LLP agreement. |

|

21 |

Authority in conduct of business |

Individual director or member does not have authority in conduct of business of company |

Every partner has authority to conduct business of LLP, unless the LLP agreement provides to contrary. |

|

22 |

Related party transactions |

Regulated under section 188 of Companies Act, 2013 |

Not regulated by the Act |

|

23 |

Accepting deposits |

Regulated by sections 73-76 of Companies Act, 2013 |

Not regulated by the Act |

|

24 |

Making loans and investments |

Regulated by section 186 of Companies Act, 2013 |

Not regulated by the Act |

|

25 |

Loans to directors / partners |

Restrictions under section 185 of Companies Act, 2013 |

No restrictions |

|

26 |

Remuneration |

Restrictions on remuneration to director as per Companies Act, 2013 |

No restriction on remuneration to partner. Remuneration should be as per the provisions of LLP agreement which may be subject to limits under Income-tax Act. |

|

27 |

Requirement of specific management |

Specified companies to have independent directors, women directors, key managerial personnel, audit committee, nomination and remuneration committee, etc. |

No such requirement |

|

28 |

Corporate social responsibility (CSR) |

Mandatory CSR provisions for specified companies |

No CSR provisions |

|

29 |

Change in name and address of members / partners |

No legal requirement to intimate change of name and / or address by a member |

Every partner has to intimate change of name or address to LLP within 15 days in Form No. 6. LLP also has to file the details with Registrar within 30 days of change in Form No. 4. |

|

30 |

Notice of resignation of director |

Notice of change of director is to be given by company in DIR-12. A director who has resigned has also to file Form DIR-11 to RoC |

A partner who has resigned from LLP can himself file notice of his resignation to RoC in Form No. 4 |

|

31 |

Shares, allotment, etc. |

Share, share certificate, register of members, transfer and transmission of shares, etc., is required |

No requirement of share and share certificate. Hence, no question of its issue, allotment, transfer, etc. |

|

32 |

Return on capital |

Paid as dividend to shareholders. No interest is payable on capital to shareholders |

Profits can be withdrawn by partners as per LLP agreement. Also interest can be paid on contribution if LLP agreement allows so. |

|

33 |

Charges |

Charges are required to be registered |

Not mandatory for registration of charges. Only statement of accounts and solvency requires the information if any charge is registered. |

|

34 |

Records and registers |

Elaborate records and registers are required to be maintained |

No records and registers have been prescribed. |

|

35 |

Fraud, penalties and Prosecution |

Fraud defined in the Act. Heavy penalties and prosecutions. More than 80 provisions for imprisonment. Class action provided. |

Lesser penalties and prosecution. No class action. Fraud not defined. |

|

36 |

Oppression and mismanagement |

Elaborate provision relating to redressal in case of oppression and mismanagement |

No provision relating to redressal in case of oppression and mismanagement |

|

37 |

Nidhis / NBFCs |

Specific provisions relating to Nidhis / NBFC |

No specific provisions relating to Nidhis / NBFC |

|

38 |

Financials |

Annual financial statements to be filed. |

Statement of accounts and solvency is to be filed annually. |

|

39 |

Not for Profit Organizations |

Can incorporate section 8 company for NPO activities |

Not allowed to incorporate LLP for NPO activities |

|

40 |

Conversion |

A private limited company and a unlisted public company can be converted into LLP under LLP Regulations |

A LLP can be converted into a company under Companies Act, 2013 |

|

41 |

Rate of Income tax |

Domestic companies - For AY 2016-17 - 30% plus 3% cesses. Surcharge 7% if total income exceeds Rs. 1 Crore but is below Rs. 10 Crore. Surcharge is 12% if income exceeds Rs. 10 Crore. |

For AY 2016-17 - 30% plus 3% cesses. Surcharge 12% if total income exceeds Rs. 1 Crore. |

|

42 |

Residential status |

If it is Indian company or the control and management of company is situated wholly in India then it would be resident in India |

If control and management of a LLP is situated wholly outside India then it would be non-resident. |

|

43 |

Applicability of accounting Standards |

Company (Accounting Standards) Rules, 2006 or to specified companies w.e.f. 1st April 2017 Indian Accounting Standards (Ind AS). Secretarial Standards for minutes. |

Accounting Standards issued by ICAI. |

|

44 |

MAT / AMT under Income-Tax Act, 1961 |

Minimum alternative tax under section 115JB applicable |

Alternative minimum tax under section 115JC applicable |

|

45 |

Remuneration to directors / partners |

Remuneration allowable would be as per appropriate resolutions passed, there is no specific restriction under Income- tax Act |

Remuneration allowable would be as per LLP agreement subject to compliance and limits mentioned in section 40(b) of Income- tax Act, 1961 |

|

46 |

Interest to directors/ partners |

Interest allowable would be as per appropriate contracts/agreements for taking of loans, there is no specific restriction under Income- tax Act,1961 |

Interest allowable would be as per LLP Agreement subject to compliance and limits mentioned in section 40(b) of the Income- tax Act,1961 |

|

47 |

Dividend Distribution Tax |

Applicable @ 15% plus surcharge @ 12% and cesses under section115-O of Income-tax Act, 1961 |

Not applicable |

|

48 |

Liability of directors / partners for tax dues in case of liquidation |

Every director is jointly and severally liable unless he proves non-recovery cannot be attributed to his gross neglect, misfeasance or breach of duty – Section 179 of Income -tax Act, 1961 |

Every partner is jointly and severally liable unless he proves non-recovery cannot be attributed to his gross neglect, misfeasance or breach of duty – Section 167C of Income -tax Act, 1961 |

From the above comparison a person may easily come to a conclusion that for a small and medium enterprise doing business in form of LLP is much easier than doing as a company. Due to this, the law related to LLP, its formation, conversion, operation and taxation has gained immense importance.

GST Slab Rates in India

GST stands for goods and services tax, Govt. aims to implication of GST for one nation one tax. Goods and services tax is a tax levied on goods and services imposed at each point of sale or rendering of service. Such GST could be on entire goods and services or there could be some exempted class of goods or services or a negative list of goods and services on which GST is not levied.

GST is an indirect tax in lieu of tax on goods (excise) and tax on service (service tax). The GST is just like State level VAT which is levied as tax on sale of goods. Goods and services tax (GST) will be a national level value added tax applicable on goods and services.

Recently GST council sets different tax slab rate for various types of goods and services under GST regime. As soon as the GST slab was declared a great importance of wave filled with curiosity hits across the industries and traders. Here you can find out the 5 slab rates under 4 categories of GST in India.

|

Commodities, Services |

GST RATE |

|

Essential farm produced mass consumption items like milk, cereals, fruits, vegetable, jaggery (gur), food grains, rice and wheat |

NIL |

|

Sleeper, metro tickets and seasonal passes |

NIL |

|

Common use and mass consumption food items such as spices, tea, coffee, sugar, vegetable/ mustard oil; newsprint, coal and Indian sweets |

5% |

|

Airlines (Economy class) |

5% |

|

Railways (AC) |

5% |

|

Railway freight |

5% |

|

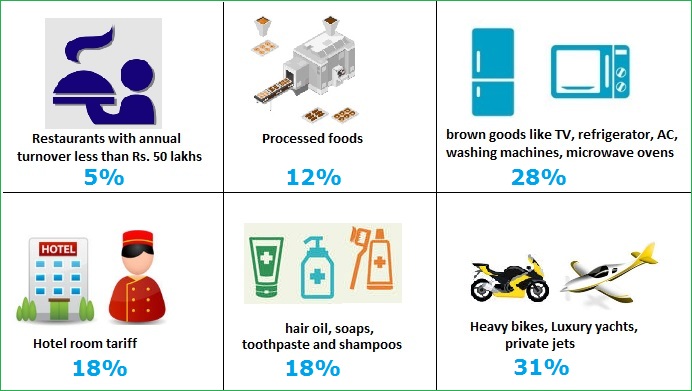

Restaurants with annual turnover less than Rs. 50 lakhs |

5% |

|

Cab aggregators like Ola, Uber |

5% |

|

Processed foods |

12% |

|

Hotels with tariff Rs. 1,000 - 2,500 |

12% |

|

Fruit juices, live animals, meats, butter & cheese |

12% |

|

Non-AC restaurants without liquor license |

12% |

|

Work Contracts |

12% |

|

Airlines (Business class) |

12% |

|

Mobile phones |

12% |

|

All FMCG goods like hair oil, soaps, toothpaste and shampoos; chemical and industrial use intermediaries |

18% |

|

Telecom, financial service |

18% |

|

Hotel room tariff Rs. 2,500 - 5,000 |

18% |

|

AC restaurants with liquor license |

18% |

|

LPG stoves, military weapons, electronic toys |

18% |

|

White and brown goods like TV, refrigerator, AC, washing machines, microwave ovens; soft drinks and aerated beverages |

28% |

|

Cinema halls, Race clubs |

28% |

|

5 star hotels |

28% |

|

Perfumes, revolver, pistols |

28% |

|

Small cars – petrol driven |

28% + 1% cess |

|

Small cars – diesel driven |

28% + 5% cess |

|

Luxury cars |

28% + 15% cess |

|

Luxury and de-merits goods and sin category items e.g. tobacco, pan masala |

28% + cess |

|

Heavy bikes, Luxury yachts, private jets |

31% |

|

Gold, Packaged foods, cigarettes, footwear and textiles |

Likely to be announced on June 3 2017 |

For more details of GST registration in Bangalore click here

GST Council Sets New Tax Rates for Products and Services

In its most recent meeting at Srinagar, the Goods and Services Tax (GST) Council of India set the rates for the new tax structure that is expected to roll out from July 1. The meeting was attended by representatives from Indian Government as well as the state governments. At the meeting the rates for various products were decided as well and it is expected that as a result of this the prices of several products and services would come down too. Happily enough, most of these products are used for the purpose of mass consumption. The idea behind the entire effort is to make sure that GST taxes do not have an inflationary effect.

Rates finalized

The council finalized the rates of 1211 items. 81% of these were subjected to the second-highest levy of 18%. As the council stated to the media no increased burden was put on the commodities. In fact, as far as a number of commodities are concerned, the tax rates have reduced significantly and it is expected that the additional taxes imposed on regular taxes will go away as well. This would in the end serve to lower the financial burden associated with those goods and services as well.

What is the government thinking?

The government hopes that by bringing into play the GST it would be able to check ills such as evasion and also make tax collection a much-more buoyant process. As per Mr Arun Jaitley, the Union Finance Minister of India, the council has opted to reduce the tax incidence on products of daily use such as sugar, tea, coffee, sweets and some other consumer durables too. However, it has opted to make sure that cars remained as expensive as before. Bikes, whose engine capacity is greater than 350 cc, are seen as luxury goods and as such they have been levied with a new cess of 3%.

Exemptions

Exemptions have been granted to products such as food grains. This is expected to make it easier for the common people since now thanks to various levies they have to pay an additional 5% on these goods. As per Hasmukh Adhia, the Union Revenue Secretary, automobiles will be subject to a tax rate of 28%. An extra cess of 15% will be imposed on luxury cars. In the same way, the small cars that run on petrol will be facing a cess of 1% and the small cars that are powered by diesel the cess will be 3%.

Reduction in tax incidence

In case of certain goods such as hair oil, soaps, and toothpaste, the rate of tax incidence has come down to 18% from around 28%. The tax incidence on coal has also been reduced to 5% from 11.69% and this is expected to reduce the cost of power. Refrigerators and washing machines are also going to become less expensive as well. The tax rates on these have come down to 28% from 31-32%. Instant coffee and tea are expected to be put in a different bracket as well.

What are the Steps to Setup a New Startup Company in Bangalore?

One of the first things that you need to do in order to start a startup in Bangalore is get your ideas assessed by a venture capital firm. However, you need to do this only when you are looking for a business model that is based on funding.

If you wish to work on your own, you can get in touch with groups such as Startup Studios and use their services to carry out their ideas. Apart from that, there are companies in Bangalore that help startups. They can help you create your company. They can help you conceive an idea and then produce it.

The Best Part Of It All

Company registration in Bangalore has become pretty easy. Nowadays, government of India is giving priority to start new businesses and focusing on startup creation with lesser time and minimal process. The best part of all this is that you do not have to resign from your job even as your company is being formed. You can run your business alongside the job. Because, normally the whole process needs around a year to be completed to standout your niche.

These companies help you in the initial stages to assess how viable your business idea is. They define the criteria for achieving success with your concept in markets within India as well as outside. They also explore avenues for making your idea successful from the point of view of e-commerce.

Getting Started

You should know how to register a company. These companies, in a nutshell, help you get off the ground. With the help of these companies it is indeed possible to get to a stage where your idea can start to become profitable at the market stage.

At this stage, you can easily resign from your present position and start with your company. All this while, you can also keep funding your startup in a passive manner from the salary that you are earning from your present job.

The Benefits

You can register a company in Bangalore quite easily these days. The benefit of such services is that you can plan your future – from the time that you start conceptualizing till the point when you take the company over from the startup assistance firms.

As far as ideation for a startup in Bangalore is concerned there are a few things that you need to keep in mind. First of all, there are already plenty of such entities in the Garden City. This means that you already have plenty of competition. So, what should you do in order to ensure that you get off to a good start?

The Ideation Process

For starters, you need to find an area that is still virgin territory. Think of a problem that people have and one that is yet to be solved. Try focusing your energies in those areas. There are some simpler ways of getting started as well. You can always start with what you have.

In this day and age, if you are waiting you are basically wasting your time. There will never be a time when everything would be perfect. Successful people always act quickly while ones who fail are always busy deliberating. You should know the procedure to register a company in Bangalore Karnataka or can take help from good and experienced consultant.

_______________________________________________________

Related Articles

- Startup India - All the Necessary Details

- Guidelines for Company Registration in Bangalore

- Why Are Most Entrepreneurs Opting for Private Limited Company?

Registrar of Companies (ROC) in India – BusinessWindo

The Registrar of Companies (ROC) is the offices under the Ministry of Corporate Affairs in India situated in different States and Union Territories has power to primary duty of registering companies like private, public, one person, Nidhi companies, NGO and Limited Liability Partnerships (LLP) into their respective states and union territories registrar office. Registrar of Companies (ROC) offices are setup under Section 609 of the companies act, 1956 and 2013. The functions of ROC is to maintain the company registration records, financial details, company status, collect fees and offers to access specific details of the companies at a prescribed fee.

The registrar of company takes look after your company registration or company incorporation in India and deals with reporting and regulation of companies and their directors and shareholders. These offices supervise the government announcement in various interests including the annul filing of various documents.

Address and Contact Details of Registrar of Companies (ROC) in India

ROC in ANDHRA PRADESH & TELANGANA

Sh. N. Krishnamoorty (ROC Hyderabad)

2ND Floor, Corporate Bhawan,

GSI Post, Tattiannaram Nagole, Bandlaguda

Hyderabad - 500 068

Phone: 040-29805427/29803827/29801927

Fax: 040-29803727

ROC in ASSAM, MEGHALAYA, MANIPURA, TRIPURA, MIZORAM, NAGALAND & ARUNACHAL PRADESH

Shri. Chandan Kumar (ROC Shillong)

Morello Building ,

Ground Floor

Shillong - 793001

Phone: 0364-2504093

ROC in BIHAR & JHARKHAND

Sh. U.S Patole (ROC Patna)

Maurya Lok Complex, Block A

Western Wing, 4th Floor,

Dak Banglow Road

Patna - 800001

Phone: 0612-222172

Fax: 0612-222172

Sh. C.M. Karl Marx (ROC Ranchi)

House No-239 , Road No-4

Magistrate Colony, Doranda

Ranchi: 834002, Jharkhand

Phone: 0651-2482811/2480801

ROC in CHATTISGARH

Sh. R.K. Sahu (ROC cum OL for Bilaspur )

Ist Floor,

Ashok Pingley Bhawan,

Municipal Corporation,

Nehru Chowk, Bilaspur- 495001

Chattisgarh

Phone: (07752)-250092(D),250094

Fax: (07752)- 250093

ROC in DELHI & HARYANA

Sh. Rakesh Kumar Tiwari(ROC Delhi)

A) 4th Floor, IFCI Tower,

61, Nehru Place,

New Delhi - 110019

Phone: 011-26235707, 26235708, 26235709

Fax: 011-26235702

For Physical Verification of Documents:

B) Plot No. 6,7 & 8,Basement,

IICA Campus, Sector-5, IMT-Manesar,

Gurgaon, Haryana

Phone : 124-2291520

ROC in GOA, DAMAN & DIU

Sh. V. P. Katkar (ROC Goa)

Company Law Bhawan

EDC Comlex, Plot No. 21

Patto, Panaji, Goa-403 001

Phone/Fax(Off) 0832-2438617 / 2438618

ROC in GUJURAT

Sh. Vijay Khubchandani (ROC Ahmedabad)

ROC Bhavan , Opp Rupal Park Society,

Behind Ankur Bus Stop,

Naranpura, Ahmedabad-380013

Phone: 079-27437597,

Fax 079-27438371

ROC in JAMMU AND KASHMIR

Sh. O.P. Sharma (ROC cum OL J&K)

Hall No.405-408,

South Block, Bahu Plaza,

Rail Head Complex,

Jammu - 180012

Phone: 0191-2470306

Fax: 0191-2470306

ROC in KARNATAKA

Sh. M. JayaKumar (ROC Bangalore)

'E' Wing, 2nd Floor

Kendriya Sadana

Kormangala, Banglore-560034

Phone: 080-25633105 (Direct),

080-25537449/25633104

Fax: 080-25538531

ROC in KERALA

Sh. A Sehar Ponraj (ROC Ernakulam)

Company Law Bhawan, BMC Road

Thrikkakara

Kochi - 682021

Phone: 0484-2423749/2421489

Fax: 0484-2422327

ROC in MADHYA PRADESH

Sh. J.N. Tikku (ROC Gwalior )

3rd Floor, 'A' Block, Sanjay Complex

Jayendra Ganj, Gwalior

Phone: 0751-2321907

Fax: 0751-2331853

ROC in MAHARASTRA

A) Mumbai

Sh. S.P Kumar (ROC Mumbai)

100, Everest,

Marine Drive

Mumbai - 400002.

Phone: 022-22812627/22020295/22846954

Fax: 022-22811977

B) Pune

Smt. Vijaya Khandare(ROC Pune)

Registrar of Companies

PMT Building ,

Pune Stock Exchange,

3rd Floor, Deccan Gymkhana,

Pune-411004

Phone: 020-25521376

Fax: 020-25530042

ROC in ORISSA (ODISHA)

Sh. A.K. Mahapatra (ROC Cuttack)

Corporate Bhawan, 3rd Floor,

Plot No. 9 (P), Sector : 1,

CDA, Cuttack : 753014

Phone: 0671-2365361, 2366958, 2366952,

Fax: 0671-2305361

ROC in PUDUCHERRRY

Ms. S.R. Radhika (ROC Puducherry)

No. 35 First Floor

Elango Nagar

Puducherry - 605011

Phone: 0413-2240129

ROC in PUNJAB, CHANDIGARH

Sh. Santosh Kumar (ROC Chandigarh )

Corporate bhawan, Plot No.4 B,

Sector 27 B, Madhya Marg,

Chandigarh - 160019

Phone: 0172-2639415,2639416

Fax: 0172-2639416

ROC in RAJASTHAN

Sh. Sanjay Kumar Gupta (ROC Jaipur)

Corporate Bhawan

G/6-7, Second Floor, Residency Area

Civil Lines, Jaipur-302001

Phone: 0141-2222465,2222466

Fax: 0141-2222464

ROC in TAMIL NADU

Shri Sridhar Parmarthi

A) Chennai

Block No.6, B Wing 2nd Floor

Shastri Bhawan 26,

Haddows Road,

Chennai - 600034

Phone: 044-28270071

Fax: 044-28234298

B) Coimbatore

Sh. N.Ramanathan (ROC Coimbatore)

Registrar of Companies

Stock Exchange Building, II-Floor,

683, Trichy Road, Singanallur,

Coimbatore - 641 005

Tamilnadu

Phone: (0422) - 2318170 (D), 2318089, 2319640

Fax: (0422) - 2318089

ROC in UTTAR PRADESH & UTTARAKHAND

Sh. Puneet Duggal (ROC Kanpur & Nainital)

37/17, Westcottt Buidling,

The Mall,

Kanpur-208001

Phone: 0512-2310443, 2310227, 2310323

ROC in WEST BENGAL

Sh. B. Mohanty (ROC Kolkata)

Nizam Palace

2nd MSO Building

2nd Floor, 234/4, A.J.C.B. Road

Kolkata - 700020

Phone: 033-2287 7390

Fax 033-22903795

All You Need To Know About Professional Tax in India

If you look at your pay slip you will see that there is a small amount that has been deducted along with all the basic breakups in your salary, house rent allowance, travel, and other areas. Normally, the amount deducted in this case is in the region of INR 200 for Karnataka and is referred to as professional tax.

This tax is not the same in each and every state in India. Means it differs from state to state. In certain States and Union Territories, you would see that no money is deducted as professional tax. Means till now, they haven't imposed it and don't want to entail into their region. This is why you may want to know what professional tax is.

What is professional tax and who imposes it?

Professional tax is a tax levied on monthly gross salary of one’s income. This is a statewide tax, applicable to the person’s or professional’s income. If he/she meets the certain monthly income range then the person or professional has liable to pay it.

The state has the power to imply this tax to the people those who are working inside the region of state and territory. Remember this tax is not implied by the nation. It's state's own tax structure.

Who has to collect and pay professional tax?

Professional tax is normally collected by the state and is applicable for all individual professionals who are earning in the state. And this tax would be deducted from employee salary account by the employer and submitted to state Govt. tax department.

Who all are taxed for PT?

Professional tax (PT) registration is an important part of state taxes. The purpose of this tax it is to collect from the professionals through employer and use it in developmental work. It is important that you do not get confuse the word "professional" they might be the people such as doctors, engineers, chartered accountants, company secretaries, etc. and others.

This tax needs to be paid by every person who earns a certain amount montly as per the state rule. Normally, the upper limit for these taxes is around INR 2500 per year. This is constant in spite of the fact that the rates vary from one state to another.

Differences and reasons on professional tax

One of the major reasons for the variation in this tax is the fact that the state governments charge this tax and as such there are always going to be differences. Each and every state that levies this tax declares a slab and the rate of tax is collected based on the below said slabs.

In some states and union territories the tax does not exist at all. It is normally computed by dividing the yearly professional tax into 12 equal installments. Normally you pay the most in February since it has the least number of days in a year.

Source of income for individual or organization

In certain states the source of your income could itself make you liable to be subjected to other taxes. In some states for example if you are running a transport business you have to pay a professional tax of INR 50 per year. The maximum limit in this case is INR 1000.

Professional tax is normally collected by your employers and is deducted from the salary they pay you every month. Having collected them the employers are supposed to deposit it with the government. If they fail to do this – for whatever reason it may be – they can be subjected to penalties.

If you are thinking about Karnataka profession tax, nowadays e-Prerana is making quite easier these days to do professional tax registration in Karnataka seamlessly .

What does self-employed person do for PT?

If you are working as a solopreneur or freelancer for yourself then it is your responsibility to pay the said tax by yourself. You can easily register yourself and apply for professional tax registration online. This application can be done by way of a form.

Once the government gets the form it will issue a registration number for you. With the help of these registration numbers you can pay professional tax in the banks as well. You can try and find out if there are any benefits related to paying these taxes and avail them.

PT slabs rate levied by major states

The following are the various professional tax slab rates in India for most growing cities of different states.

Professional tax rate in Mumbai, Maharashtra

|

Monthly Salary |

Monthly Payable Professional Tax |

|

Up to Rs. 7,500 (For Male) |

Nil |

|

Up to Rs. 10,000 (For Female) |

Nil |

|

Rs. 7,501 to Rs. 10,000 (For Male) |

Rs. 175 per month |

|

Above Rs. 10,000 (For both Male & Female) |

Rs. 2,500 annually |

Professional tax rate in Kolkata, West Bengal

|

Monthly Salary |

Monthly Payable Professional Tax |

|

Up to Rs. 10,000 |

Nil |

|

Rs. 10, 001 to Rs. 15,000 |

Rs. 110 |

|

Rs. 15,001 to Rs. 25,000 |

Rs. 130 |

|

Rs. 25,001 to Rs. 40,000 |

Rs. 150 |

|

Above Rs. 40,000 |

Rs. 200 |

Professional tax rate in Bangalore, Karnataka

|

Monthly Salary |

Monthly Payable Profession Tax |

|

Up to Rs. 15,000 |

Nil |

|

Above Rs. 15,000 |

Rs. 200 |

Professional tax rate in Hyderabad, Telangana

|

Monthly Salary |

Monthly Payable Profession Tax |

|

Up to Rs. 15,000 |

Nil |

|

Rs. 15,001 to Rs. 20,000 |

Rs. 150 |

|

Above Rs. 20,000 |

Rs. 200 |

Professional tax rate in Andhra Pradesh

|

Monthly Gross Salary |

Monthly Payable Profession Tax |

|

Up to Rs. 15,000 |

Nil |

|

Rs. 15,001 to Rs. 20,000 |

Rs. 150 |

|

Above Rs. 20,000 |

Rs. 200 |

Professional tax rate in Chennai, Tamil Nadu

|

Half Yearly Gross Income |

Profession Tax Payable Half Yearly Basis |

|

Up to Rs. 21,000 |

Nil |

|

Rs. 21,001 to Rs. 30,000 |

Rs. 135 |

|

Rs. 30,001 to Rs. 45,000 |

Rs. 315 |

|

Rs. 45,001 to Rs. 60,000 |

Rs. 690 |

|

Rs. 60,001 to Rs. 75,000 |

Rs. 1,025 |

|

Above Rs. 75,000 |

Rs. 1,250 |

Professional tax slab rate in Ahmedabad, Gujarat

|

Monthly Salary/Wages |

Monthly Payable Profession Tax |

|

Up to Rs. 5,999 |

Nil |

|

Rs. 6,000 to Rs. 8,999 |

Rs. 80 |

|

Rs. 9,000 to Rs. 11,999 |

Rs. 150 |

|

Rs. 12,000 or above |

Rs. 200 |

States & Union Territories have not levied professional tax?

See the table below herein, list of states and union territories that are not charging tax on profession who are doing jobs in their cities or regions.

|

States Not Charges Profession Tax |

Union Territories Not Charges Profession Tax |

|

Arunachal Pradesh |

Andaman and Nicobar Islands |

|

Goa |

Chandigarh |

|

Himachal Pradesh |

Daman and Diu |

|

Haryana |

Dadra and Nagar Haveli |

|

Jammu and Kashmir |

Delhi (National Capital Territory) |

|

Punjab |

Lakshadweep |

|

Rajasthan |

|

|

Uttar Pradesh |

|

|

Uttarakhand |

|

Is professional tax mandatory?

Yes, professional tax is compulsory for professionals. If a person is earning an income from his/her profession and meets the monthly taxable income range then he/she has to pay it.

Is professional tax applicable for contract employee?

Professional tax is not applicable for contract employee, because they don’t have employer and employee relationship. But TDS can be applicable to them, if they come under that area.

What is the due date for payment of professional tax?

Due date for professional tax in India is payable on or before 20th of every consequent month that could be based on the state government’s tax rule. And annual statement has to file before 30th May of every financial year.

------------------------------------------------

Also Read:

Chartered Accountant Services in Bangalore Karnataka

How to Claim Income Tax Refund: A Step by Step Guide

Annual Return Filing for Companies under the Compliance of 2013

Startup India – All the Necessary Details

The Startup India Stand up India event was organized by the Indian Government under the aegis of Narendra Modi, the Prime Minister of India, on 16th January 2016. In a way this event encapsulated all the benefits for starting an ecosystem of startups in India. Such an event had a significant amount of importance considering how it was the first time that the national government and the startup community in India were coming into contact with each other and interacting on key issues. The very programme – Startup India – can be deemed a flagship effort on part of the central government.

What does this programme intend to do?

The Startup India plan is supposed to create a strong ecosystem where innovation can be nurtured and more startups can be had. This is expected to lead to a level of economic growth that can be sustained over the long time, and also lead to employment on a huge scale. The national government – through this programme – aims to empower these budding business units in such a way that they can chart their own course of innovation and grow in the way that they wish to. In order to satisfy the aim behind this programme an Action Plan has been created by the Government of India.

Action Plan

This Action Plan deals with each and every aspect of the startup ecosystem in India. By using this plan the government is hopeful that it will speed up the startup movement in the country. At present such companies are only limited to the technology and digital sector but the national administration wants it to spread to other sectors as well such as agriculture, healthcare, manufacturing, education and social sector. From a geographical point of view these are restricted to the tier 1 cities but the government is hopeful that the semi-urban and rural areas will come in its fold as well.

Compartments of the action plan

The action plan has been divided into several areas. Some of them may be mentioned as follows – simplification and handholding, industry-academic partnership and incubation, and funding incentives and support. A lot of entrepreneurs in India may be thinking if their venture would be deemed worthy of assistance under the new project or not. The Department of Industrial Policy and Promotion (DIPP) of the Indian Government has provided the definition of startups and thus made it clear as to which companies will be considered eligible for assistance under the programme.

The necessary criteria

The said company must be incorporated and registered in India. It should not be older than five years. Its annual turnover should have never been more than INR 25 crore in any of the years that it has been functional. The company should be focusing on innovating, developing, deploying, and commercializing new products, services, and processes that are technology driven in nature. It is also important that the company applying for the benefit has not been formed by reconstructing or splitting up a company that existed before. If a company has been older than 5 years or if it has ever earned more than INR 25 crore a year it will not be regarded as a startup any more.

Concept of One Person Company Explained for Young Entrepreneurs

The concept of one person company was introduced in India by the Companies Act, 2013. Ever since its introduction it has been deemed a revolutionary thought. It was an expert committee led by Dr. JJ Irani that recommended the said concept. For people looking to kick off their own businesses with a proper and organized structure the concept of One Person Company opens up some whole new opportunities. With such a company, as a young entrepreneur you will get all the benefits that are normally associated with a private limited company. This categorically implies that they will be able to access credits, business protection in a legal manner, bank loans, market, and enjoy limited liability as well.

Background of this business

As a concept, one person company registration may be a new one in India. However, it has been in existence – and also achieved a fair degree of success, it must be said – in the United Kingdom as well as several other countries across Europe. In fact, this form of business has been in existence for a significant period now. The concept itself has some special features that have been mentioned in the Sub Section 62, Section 2, The Companies Act 2013.

What is a One Person Company?

A One Person Company is basically a company that has only a single member. It also needs to be noted in this context, that for all legal intents and purposes such a company is defined in legal terminology as a private company. Normally, each and every law and provision that is applicable to a private company is applicable for one person company registration in India as well, until and unless anything else is mentioned in this regard. The Companies Act 2013 has however provided an exception to the concept.

Exception to One Person Company

As per this exception, only a natural-born Indian would be able to register a One Person Company in India. That person needs to be a resident of India as well. This means that the advantages of such a company can only be availed by Indians who were born in the country and are staying in it as well. Alongwith this, it needs to be mentioned that the upper limit for forming such a company has been limited to 5 for each individual. Now, you may want to know how such a company is formed.

How to form a One Person Company

Normally, these companies are incorporated as private limited companies that only have a member each. Such companies normally have restrictions on inviting the public for subscribing to the securities held by the said company. These companies have some salient features such as limitation by guarantee, and limitation by shares. In case such a company is limited by shares there are some more restrictions that will apply to the same. For example it should have a minimum paid-up capital of INR 1 lakh. There are also restrictions on the number of shares to be held by the company. You can look up the internet for answers to this question - How can I register an One Person Company (OPC)?

Reasons Why Startups and Existing Businesses Need to Register Their Companies

As a new or established business owner it is very important that you get proper return on each and every dollar that you have invested in the same. One of the many expenses that you have to make irrespective of your business status is registering the company. At the time when you are starting your business such an expense may not seem to be that necessary but such a thought may be absolutely wrong. There are several reasons for that as well. For starters, with company registration you will be in a much-better position with regards to protecting your assets.

Protection of assets

It is always your dream to start your business but in business there is always a chance that you could lose the very assets that are holding you up in the first place. This could affect your family as well. In case, your business fails you may have no option but sell those assets in order to cover your losses. Quite often when a business fails people are sued and there are various financial issues as well. However, with company registration in India your assets can never be affected by your liabilities. There are plenty other reasons as well for registering your business but this seems to be the most important of all.

Securing your product

When you think of it calmly enough this is another reason why one should register a company. It could be that you have invented a product that is groundbreaking to say the very least. It is also possible that your product right now is being sold to millions across the country and has the potential to be sold outside it as well. This also means that your business is heading to the level that you may have envisaged for it. However, what happens when one of your customers faces a serious issue thanks to your product.

In that case there is always a chance that you could have to recall all your products and that could be accompanied by lawsuits as well. Worst of all, this could happen within the space of a night itself. By the time, the dust settles you may have become bankrupt or you may have spent every last bit of your insurance as well as savings. This is why you should go for online company registration. There are some benefits of completing such processes as well.

Satisfying monetary requirement

In case you are looking for private equity it is very important that you are registered as a business. When your company is incorporated the investors will feel a sense of security about things and would be able to pump in money in your company as well. If you have a proper exit strategy in plan then you can be sure that investors would be further impressed as well and that would increase your chances of receiving better investment. Normally these exit strategies are mentioned in the documents of incorporation only. In fact, venture capitalists actually prefer to invest in such companies.